Abstract

The scarcity of task-labeled time-series benchmarks in the financial domain hinders progress in continual learning

and AI algorithm development. Addressing this deficit would foster innovation in this area.

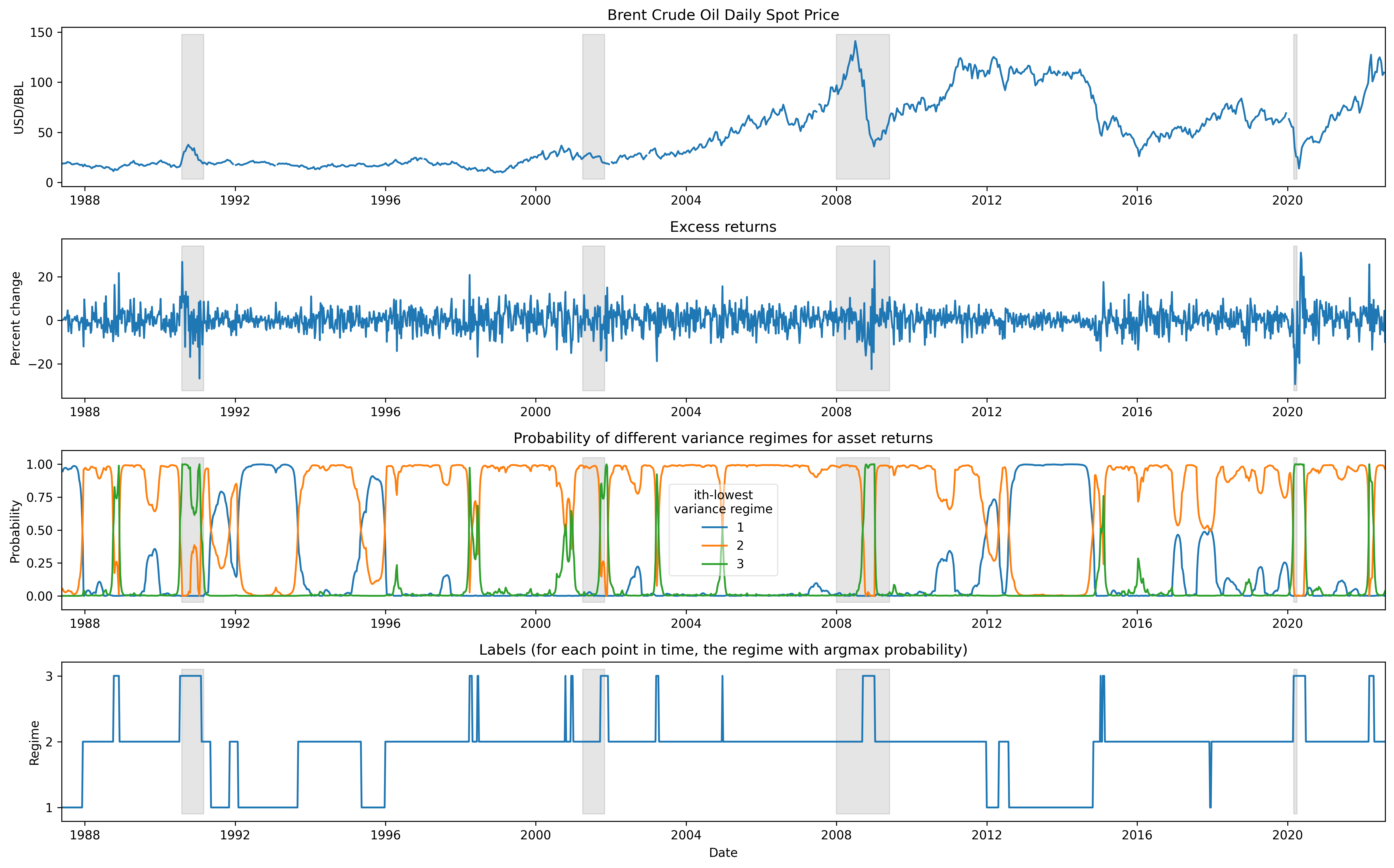

Therefore, we present COB, crude oil benchmark datasets. COB includes 30 years of

asset prices that exhibit significant distribution shifts and comes with corresponding task, or regime, labels based

on these distribution shifts for the three most important crude oils in the world: West Texas Intermediate (WTI),

Brent Blend, and Dubai Crude.

Time-series data pose challenges such as correlatedness, non-stationarity, missing data, and spurious outliers. We

address the problem of out-of-distribution detection and emphasize the relevance of our benchmarks for continual

learning.

Our contributions include creating real-world benchmark datasets by transforming asset price data into volatility

proxies, fitting

models using expectation-maximization, generating contextual task labels that align with real-world events, and

providing these labels to the public.

We hope these benchmarks accelerate research in handling distribution shifts in real-world data, in particular due

to the global importance of the assets represented by the datasets.

Download

Benchmark Datasets with Task Labels

Approach

We meticulously transform, fit the data, and transform the results to obtain labels that partition the data into task, or regimes, based on asset price volatility, a macroeconomic trend that correlates with critical global events, such as economic downturns or recessions.

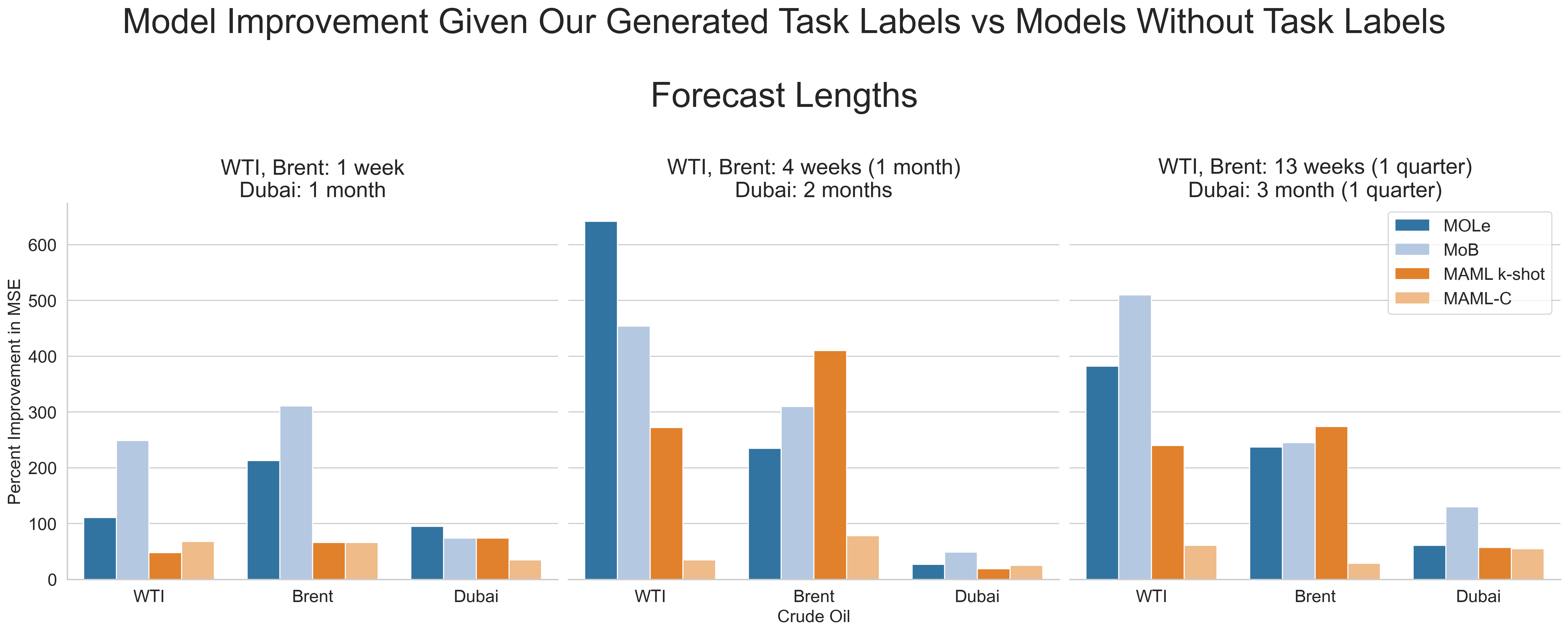

We evaluate four continual learning algorithms: (1) MOLe, (2) MoB, (3) MAML k-shot, and (4) MAML

Continuous on all three datasets.

Two of these algorithms, MoB and MOLe, instantiate new few-shot models adapted from a meta-learned prior. The two

others, MAML k-shot and MAML Continuous use a single model that is adapted from a meta-learned prior.

Results

1. The benchmark datasets (WTI and Brent resampled weekly, Dubai remained monthly) and task labels can be downloaded here.2. We report the Percent Improvement in MSE of each algorithm on each benchmark dataset over three Forecast Lengths.

- For WTI and Brent these are 1 week, 4 weeks (1 month), and 13 weeks (1 quarter).

- Since Dubai Crude data is less granular, we use Forecast Lengths 1, 2, and 3 months (1 quarter), respectively.

Conclusion

In conclusion, we have introduced three novel time-series benchmark datasets that encompass the global crude oil

market and generated task labels aligning with significant real-world events, creating a rich context for

further exploration and understanding.

Our goal is to fuel advancements in areas such as continual learning and out-of-distribution detection, while

addressing challenges posed by sequential data.

We believe that these

benchmarks, due to the societal importance of the assets they represent, can make a substantial contribution to AI

research, particularly in handling real-world data that contains distribution shifts.

As AI continues to permeate every sector, the importance of such representative, real-world benchmarks will continue

to grow.